100 Days of Conflict: Where Mortgage Rates Stand

The conflict in the Middle East has been going on for about 100 days now. And if you haven’t been connecting the dots between what’s happening over there and what mortgage rates are doing over here — this one’s for you.

(If you want the original breakdown of how this started, I walked through it back in April in Iran, the Strait of Hormuz, and Your Mortgage Rate. Consider this the 100-days-later update.)

Just a quick reminder: these articles are researched and written by me. My goal is to help you cut through the noise — beyond the headlines and soundbites.

So what does war in the Middle East have to do with your mortgage rate?

More than most people think.

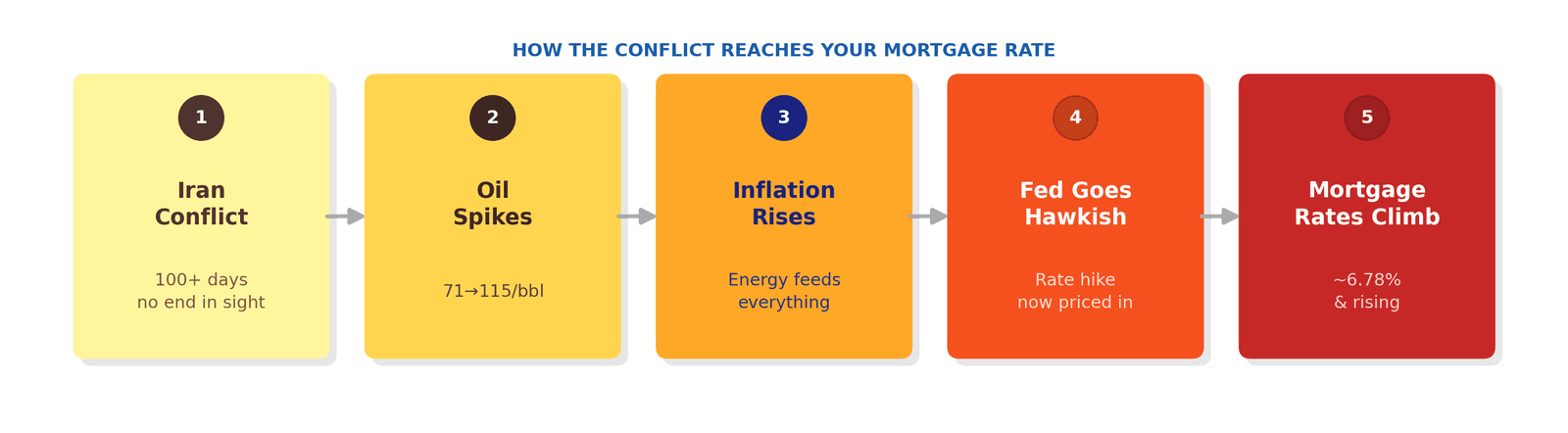

Mortgage rates don’t live in a vacuum. They track the 10-year U.S. Treasury yield — which moves based on what bond investors expect inflation to do. When oil prices rise, inflation tends to follow. When inflation rises, bond yields go up. And when bond yields go up, mortgage rates go with them.

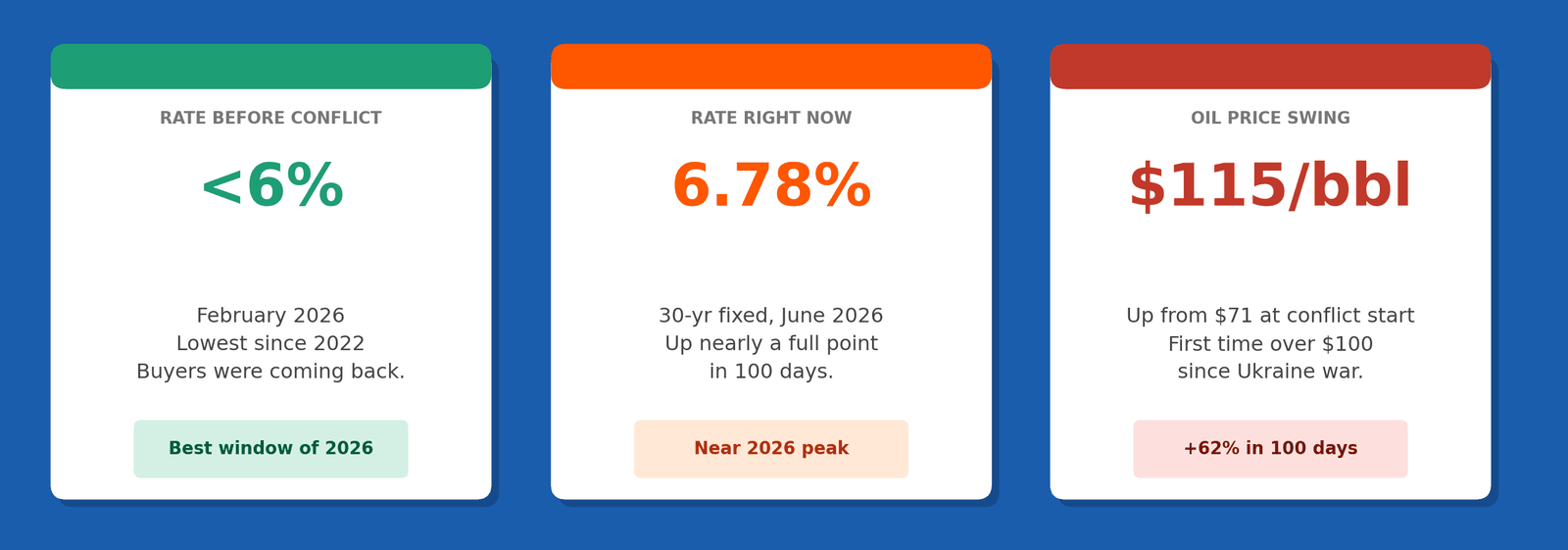

Back in February, rates had actually dipped below 6% — the lowest since 2022. Buyers were starting to come back. Then the bombs dropped. Oil shot from $71 a barrel to over $115 — the first time it crossed $100 since Russia invaded Ukraine. Inflation picked back up. Mortgage rates climbed right along with it, sitting around 6.78% today.

The question nobody wants to ask

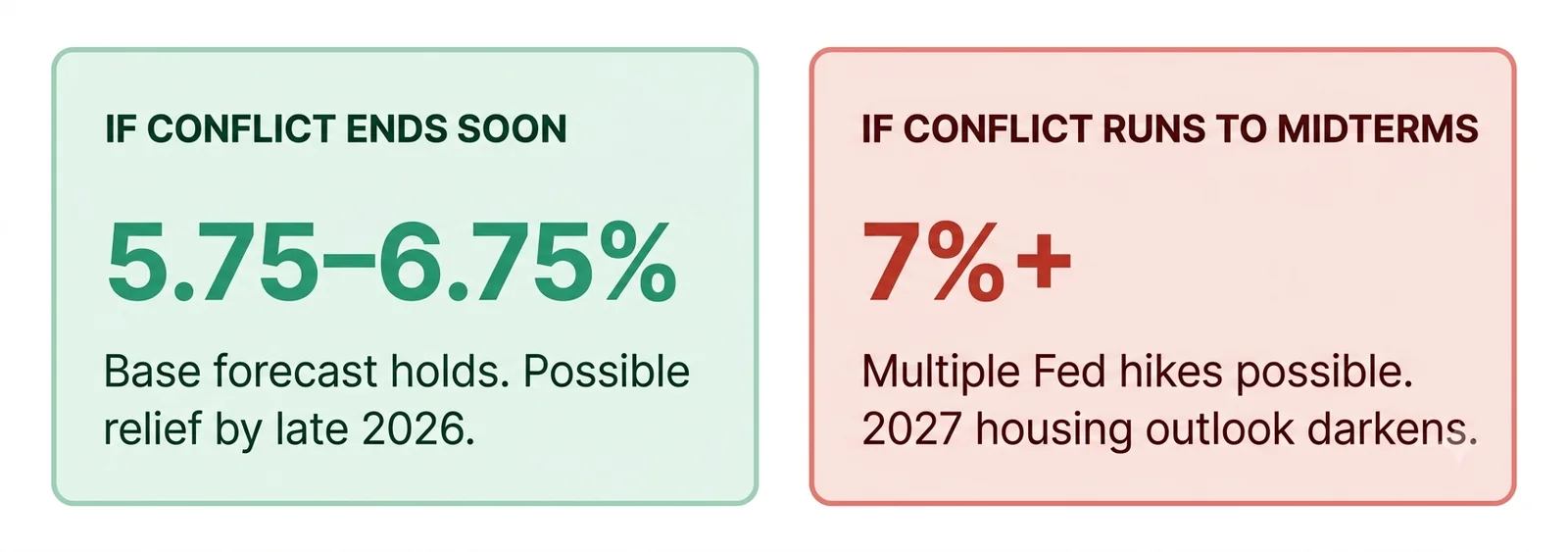

What if this doesn’t end soon?

If the conflict drags into the fall, the Federal Reserve — which was supposed to cut rates this year — may instead raise them. We’ve already gone from pricing in 2–3 rate cuts in 2026 to markets now discussing a potential hike. That’s a massive shift in just a few months.

What does this mean for you?

Waiting for rates to fall? The window we had in February — when rates touched the high 5s — may have been the best shot 2026 had to offer.

Thinking about refinancing? The wave that seemed certain back in January isn’t materializing the way people hoped. But if your current rate is above 7%, there may still be math that works.

Trying to decide whether to buy now or wait? That’s exactly why I exist. The answer is different for every family, every budget, every situation.

One bright spot: housing demand has held up better than expected. Pending sales are up 7% year-over-year. People still need places to live — and life doesn’t pause for geopolitics.

The market is stressed. But it isn’t broken.

If any of this raises questions about your situation — whether you’re buying, selling, refinancing, or just trying to figure out your next move — reach out. That’s what I’m here for.

Brian Mutter | NMLS #1109257 | Forward Mortgage NMLS #2401169

All loan applications subject to credit and underwriting approval. Not all applicants will qualify. For informational purposes only — not an offer to lend.