Where are interest rates headed in 2025?

As we enter a new year – and a new presidential administration – there is a lot of curiosity about what will happen to mortgage interest rates. Let’s dive in and unpack what may lie ahead.

Just a quick reminder: These articles I share here are researched and written by me! As part of my commitment to ongoing support for my clients and partners, I write these articles to help them understand what’s really happening in the markets, beyond the headlines and soundbites.

The foundation

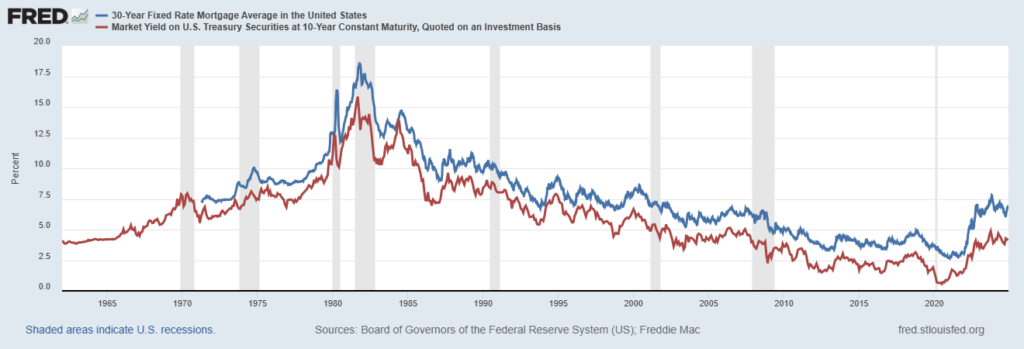

In any discussion about mortgage interest rates, it’s important to keep in mind a simple fact: Mortgage interest rates have followed the 10-year US Treasury Bond (UST10Y) for decades. While the spread between the yield of the UST10Y and mortgage rates can vary, mortgage rates have long followed the UST10Y: When the UST10Y yield increases, mortgage rates rise. When bond yields decline, so do mortgage rates.

Short story: To talk about where mortgage rates might be, we must first talk about where bond yields might be.

The current backdrop

When President-elect Trump announced his pick for Secretary of the Treasury on November 22, the bond market rallied – a hopeful sign. On that day, the UST10Y yield fell 13 basis points – that’s a big swing. To put that in perspective, from November 4 to December 2, average movement on the UST10Y was 1 to 5 basis points. (100 basis points equals one percent.) And remember, when bond yields decline, mortgage rates decline as well.

The near-future

However, we don’t expect any significant or abrupt decline of mortgage rates for the simple fact that uncertainty abounds in the US economy and the world. We’ll have a new administration in Washington, international conflicts continue in Ukraine and Russia and in the Middle East, and the labor market here in the US remains resilient.

What to watch for

With respect to some key technical levels, some analysts believe when the Initial Jobless Claims reach 323,000 on the four-week moving average, we will hit an inflection point for mortgage rates.

But we’re not there yet. Looking at the chart below, you can see that the labor market is still too strong:

In the meantime, it’s expected that the UST10Y yield will hover between 3.21 and 4.25%, which correlates to mortgage rates around 5.75 – 7.25%.

Once new jobless claims reach that critical 323k mark, it’s thought that the UST10Y could fall as low as 2.73%, which would equate to mortgages rates in the low- to mid-5’s.

What’s it all mean?

We expect rates to fall in the short- to medium-term future, BUT we don’t expect any significant changes soon.

If you’re in the market to buy a home, you should buy a home now, rather than waiting for rates to (hopefully) come down. The reasons are simple: The need to move is usually based on life-circumstances, not on the cost of borrowing money. Additionally, as rates come down, more buyers will enter the market, increasing competition, and putting upward pressure on prices.

With respect to a potential refinance, homeowners should be cautious but remain ready. Lenders will often advertise attractive low rates that come at the expense of hefty up-front fees, making the refinance less valuable. Be sure to work with a trusted advisor.

For those who bought their homes in 2022 or later, a refinance will likely make sense sometime in 2025. To be proactive, it’s best to work with your current mortgage advisor to identify an interest rate at which a refinance will make sense. From there, your advisor will monitor the market, and you can strike when the rate is right.

If you find this interesting or helpful, please feel free to share it with a friend, family member, or co-worker — it’s my goal to educate and empower as many people as possible during this incredibly unique time in housing!

Here is how I can help!

– If you are looking to purchase a new home or have questions about your mortgage, the market, getting preapproved, etc., or

– If you are a Realtor Broker, or Financial Services Professional looking for a lender with great financing solutions to help educate your clients on the state of the market to help them feel good about their decisions,

Please call today – I am happy to help however I can!

Brian Mutter is a twenty-year veteran of the mortgage and real estate industry. His vast experience across nearly all aspects of real estate makes him an incredibly well-rounded problem-solver. Brian’s clients are treated to a white-glove client experience every single time. Education, information, and communication are the cornerstones of his approach.