Credit Checks: Soft Pulls, Hard Pulls & Shopping Windows

As we head into a busier season, I thought this would be a great time to share a quick refresher on credit inquiries. This is something that comes up a lot and can be confusing if you don’t deal with it every day.

Feel free to pass this along to anyone who might find it helpful.

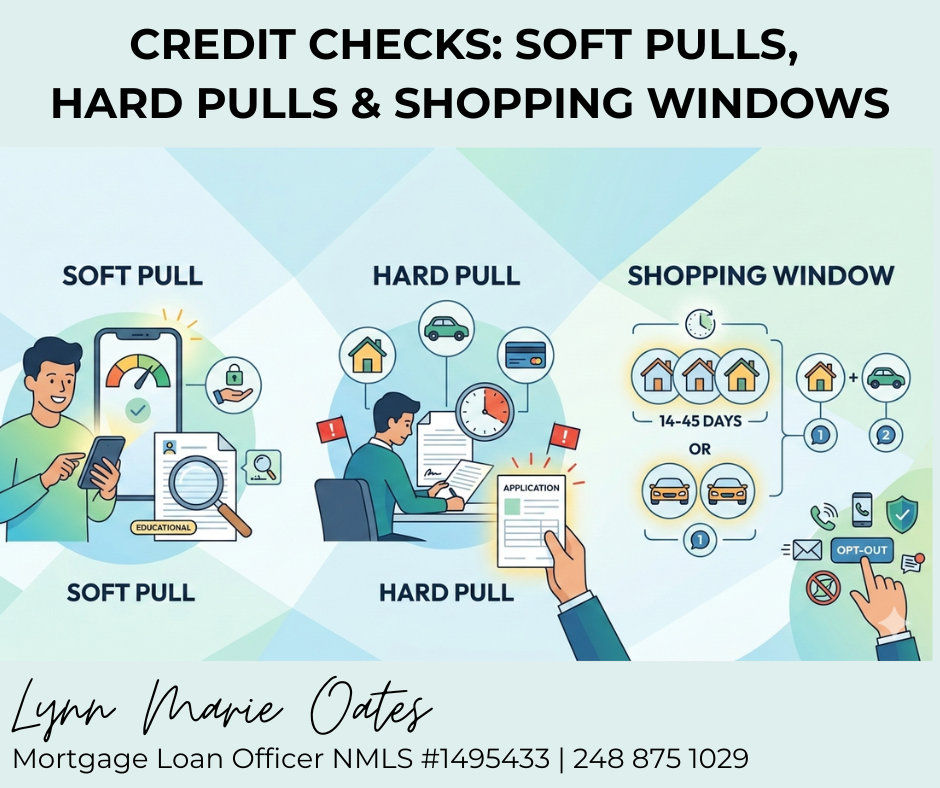

So, what’s the difference between a soft pull and a hard pull?

What is a soft pull?

A soft pull is the most common type of credit check and is what you’ll usually see on free credit monitoring sites like Credit Karma or CreditWise. A soft pull:

- Does not impact your credit score

- Is not visible to other lenders

- Is often used for educational or pre-qualification purposes

A quick note about online credit scores:

Tracking your credit score online is a really helpful habit, and I always encourage it. Just keep in mind that most free credit monitoring tools usually show a score from one credit bureau and often use a different scoring model than what mortgage lenders use. Mortgage lending typically looks at all three bureaus and uses older, industry-specific scoring models. So while your online score is a great way to spot trends and catch issues early, it’s best to take it with a little bit of salt—it’s more of a snapshot than the full picture.

What is a hard pull?

A hard pull happens when you apply for new credit, such as:

- A mortgage

- An auto loan

- A new credit card

Hard pulls are requested by lenders and are visible to other creditors. Each hard inquiry can lower your score slightly (usually 2–5 points), depending on your overall credit profile. Too many hard pulls in a short period of time can signal that you’re taking on a lot of new debt and may impact approvals.

Important Note On Hard Pulls (and Yes… This Is When the Phone Starts Ringing)

After a hard inquiry, your info can be flagged as “active,” which is usually when the unsolicited calls begin. Annoying? Yes. Expected? Also yes.

It is important to note; the credit bureaus are allowed to sell that information as a “trigger lead.” That means your inquiry alerts other lenders that you’re actively shopping for credit. Some lenders then pay for those leads and immediately reach out with calls, texts, or emails and often aggressively.

These companies are not affiliated with your lender, and many rely on urgency or pressure tactics to get your attention quickly. While not all are bad actors, this practice is often used by more predatory lenders who are paying for speed and volume, not long-term relationships. This is why opting out ahead of time can make a big difference.

- See Opt Out information below to save yourself the pain and irritation of these calls

Are shopping windows actually real?

Short answer: yes but with some fine print.

When shopping for a mortgage or auto loan, credit scoring models typically allow a “shopping window” of about 14–45 days, depending on the scoring model used. To be safe, it’s best to assume 14 days.

Here’s how it works:

- Multiple mortgage inquiries within the window usually count as one

- Multiple auto loan inquiries within the window usually count as one

- Mortgage + auto loan inquiries = two separate inquiries

This shopping window does not apply to things like credit cards or personal loans—those usually count individually.

Quick recap:

- Auto loan + auto loan (within 14 days) = 1 inquiry

- Mortgage + mortgage (within 14 days) = 1 inquiry

- Mortgage + auto loan = 2 inquiries

I hope this makes credit inquiries a little easier to understand and easier to explain to others too. If you ever have questions or want help reviewing your options, I’m always happy to help.

A Quick Tip: Don’t Skip the Opt-Out

Even though this new law is in the works, the best thing you can do right now is opt out of trigger leads yourself. It’s quick, it’s free, and it can save you a lot of stress.

Here’s how:

- Opt-Out Prescreen

This site lets you stop pre-screened offers for credit and insurance — not just for mortgages.

- It takes a few days to go into effect, so don’t wait.

- You can opt back in later if you change your mind.

- Here’s the link: https://www.optoutprescreen.com/

- National Do Not Call Registry

Another solid layer of protection. Add your number here to reduce marketing calls — including many related to trigger leads.

As always, feel free to share this with anyone who could use a little clarity around credit

Lynn Marie Oates

Mortgage Loan Officer NMLS #1495433

(248) 875-1029

lynnoates@goforwardmortgage.com

I know firsthand how overwhelming securing a mortgage can feel — and that’s exactly why I’m here. With my experience and a heart for helping people, my goal is to guide you through every step with clarity, patience, and care.

I take a personalized, relationship-first approach, offering full support and clear communication so you never feel rushed or unsure. I take the time to understand your goals, explain your options, and help you put your strongest offer forward when it matters most.

Helping people feel confident, prepared, and excited about homeownership isn’t just part of my job — it’s what I truly love to do!